Compound interest is one of the financial powers that can have a profound effect on your wealth over time. The concept of compound interest goes far beyond its mathematical assumption, implying a deeper understanding that is rooted in practical application. This financial principle, which is interest on both the principal amounts and compounded amounts of interest, has deep implications in personal finance.

Either an individual is saving with great zeal to accumulate money for retirement or investing planfully towards future endeavors, compound interest surfaces as a critical aspect that can altogether alter the course of financial growth. As opposed to simple interest, which is based only on the initial loan amount used for an investment activity, compound interest factors in both of these values. It can result in a large sum from an initial modest investment over time.

Understanding Compound Interest

Compound interest is a foundational financial principle that plays an important role in investments, savings, borrowing and overall income management. In essence, compound interest is the determination of the interest not only on initial capital but also on historical accumulation. It thus has a cumulative effect, and the formula depicts this ongoing process.

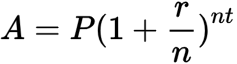

The compound interest formula is given by:

(Source: Calculator Soup, 2023)

Where:

– (A) is the future value of the investment/loan, including interest.

– (P) is the principal amount (initial investment or loan amount).

– (r) is the annual interest rate (in decimal form).

– (n) is the number of times that interest is compounded per unit (t).

– (t) is the time the money is invested or borrowed for, in years.

This formula represents the amount of money accumulated after (n) years, including interest compounded (n) times per year.

A significant aspect that affects compound interest is the frequency of compounding. If interest accrues annually, semi-annually, or quarterly as well as monthly, it tends to have a significant impact on overall growth in the investment somewhere. The higher the frequency of compounding, the greater the interest to be added on top of the principal, which results in a faster growth slope. This effect emphasizes the need to factor in compound frequency in financial decisions.

The value of time is also emphasized in the aspect of compound interest. Time is a crucial factor in the development of an investment. The effects of compounding are more pronounced when the money invested grows over a long period, which explains why it is advised to start investing early in life so as to gain maximum benefits.

Also Read: Market Maker Options: Definition and How They Make Money

A good thumb rule for measuring the rate of compound interest is known as Rule 72. It is possible to determine the approximate number of years needed for a threefold investment by dividing 72 by the annual interest rate. This rule offers a short and valuable guideline concerning how much time is required to reach particular financial objectives.

However, compound interest has diverse uses in different financial instruments. It impacts savings accounts, loans, mortgages and investment portfolios. This availability represents the ubiquity of compound interest in dictating financial practices and decisions.

Although compound interest provides an opportunity for growth at exponential rates, the risks associated with it should also be taken into account. Attachment to compound interest solely in long-term financial planning leaves a person open to market fluctuations, economic uncertainties, and changes in interest rates. Diversifying investment strategies and becoming familiar with the general financial environment can partially mitigate such risks.

Compound interest is a rather complicated financial tool that must be carefully analyzed in regards to short- and longterm monetary planning. The nature of exponential growth, which depends on compounding frequency and time, makes this phenomenon immensely crucial in determining financial structures.

Applications of Compound Interest

Compound interest, which is applied to different financial instruments, affects in various ways how individuals and groups save money. Here are some key applications:

1. Savings Accounts

In the context of savings accounts, compound interest serves as a foundation for accruing wealth and yields fruitful results in all facets. As funds are deposited into a savings account, the return on capital not only increases its principal but also multiplies the already accumulation of interest. This cumulative phenomenon makes possible exponential growth, as witnessed in the increase of people’s savings much faster than with ordinary interest. This aspect is beneficial to savers, as it benefits both short-term and long-term savings plans. It promotes saving behavior and rewards those who hold their funds deposited for a long time. In addition, knowledge of compound interest gives savers power over selecting financial institutions or accounts that offer favorable terms for the growth of their savings potential.

Apart from the individual level, banks and financial firms use compound interest to procure deposits. They provide competitive interest rates to attract people’s funds, and this creates a give-and-take relationship. Thus, the use of compound interest in savings accounts extends beyond personal finances to influence larger economic forces determining how individuals and institutions engage with each other within this financial framework.

2. Loans and Mortgages

Compound interest has a major role to play in the overall cost of loans and mortgages. In addition to repaying the original loan amount, borrowers also have to pay interest on both of them that accrues in periods before and after. This cumulative effect results in higher total repayments during the lifespan of the loan. This highlights the need for consumers to be aware of loan terms, especially interest rates and compounding interests. It also highlights the costlier effect of long-term borrowing while bombarding borrowers with how compound interest adversely affects their ability to repay.

However, creditors use compound interest to control risk and create profits. The profits from loan interest are also added to the money flow of a financial institution, and this revenue stream contributes to the company’s ability to offer several products and services. The link between borrowers and lenders is found in the relationship of compound interest rates on loans and mortgages, which highlights its importance for financial transaction’s transparency throughout this domain.

3. Investment Portfolios

Among investment portfolios, compound interest acts as an effective partner in the case of those who are interested in building their long-term wealth. Investors use the compounding effect to magnify their gains over periods of time. When investing in stocks, bonds or other financial instruments, interest earned by itself allows the investment base to grow at an incredible rate. Such a compounding dynamic is especially favorable for people who have patience and a consistent attitude towards investing because it pays off for those who stay dedicated to their investment strategies over time. The idea also promotes diversification and sound risk management, two key factors in creating resilient investment portfolios.

Understanding compound interest, however, is crucial for investors to set reasonable expectations and formulate suitable investment plans. It highlights the need to invest early in order to optimize compounding over time. Additionally, the concepts of compound interest guide decisions regarding portfolio review frequency, reinvestment tactics and the choice of investment instruments. In a wider sense, the use of compound interest in investment portfolios contributes to the functioning and development of capital markets, which form the financial world for individuals as well as institutional investors.

4. Retirement Planning

Compound interest is one of the pillars in retirement planning that steers individuals towards their financial desires at old age. By starting savings early and reaping the benefits of compounding that span several decades, people are able to accumulate large retirement funds. This not only stresses the importance of saving consistently and regularly but also addresses time as an important factor in regard to retirement savings. With the compound interest phenomenon, retirement accounts such as 401(k)s or IRAs are a source of great wealth strength that can serve one into his or her old age years.

Compound interest is beneficial to retirees because they are able to devise withdrawal strategies that satisfy both financial requirements and base preservation. The procedure for compound interest also shapes retirement saving decisions, portfolio risk exposure levels, and the timing of investment contributions. On a wider socio-economic basis, the proper utilization of compound interest in retirement planning strengthens individuals’ financial security and thus underpins the stability of retirement programs.

5. Education Savings

To finance families’ preparation for increasing costs of education, compound interest is an important part of the field of educational savings. Tools such as 529 plans use the power of compounding to help families accumulate their savings over time. With regular contributions to these education-focused accounts, parents can benefit from the great growth potential while rest assured that funds are at hand when children head off to college. This application highlights the significance of early and regular deposits into education savings funds, as compound interest greatly enhances the resources for future educational outlays.

A deeper understanding of compound interest as it relates to education savings allows families to select the best possible investment instruments and approaches. It leads to thoughts of time horizons for educational costs, risk appetite and the effect that compounding cycles have on how fast savings grow. Beyond the individual perspective, in terms of fostering societal aims such as increasing access to tertiary education and relieving barriers through finance for future generations.

Compound Interest Strategies for Maximizing Wealth

The concept of wealth maximization through compound interest is based on sound financial planning and precise implementation. Here are key strategies to leverage compound interest for wealth accumulation:

– Start Early and Stay Consistent

Starter savings and investments are key pillars of a wealth accumulation strategy based on compound interest. The discount rate is often neglected, but its influence can be profound. However, by starting the saving or investing process early in life, people let their money grow exponentially for a longer period of time. Consistency is equally vital. Small, regular contributions form part of the compound effect. The habit of the decided discipline to make regular deposits accumulates great wealth over a number of years. This approach is especially effective for more long-term financial goals, such as retirement planning or a large investment portfolio.

It further gives people the opportunity to recover in times of market downswing. This strategy is persistent in markets’ short-term movements since, over the long term, market volatility effects tend to even out. In addition, regular contributions help investors benefit from dollar-cost averaging and save money by buying fewer shares when prices rise while purchasing more shares at lower price levels.

– Optimize Compounding Frequency

One of the tactical aspects to consider in order to maximize wealth through compound interest is the frequency associated with adding an interest rate to the principal. High frequencies of compounding, such as monthly or quarterly, increase the influence of composition. This implies that interest is compounded more often, accelerating growth. Under the careful selection of savings accounts, certificates of deposit (CDs), or any other investment tool, people might consider choosing more frequently compounding ones to increase overall investing capital growth.

Balancing compounding frequency is therefore necessary. Although more frequent compounding may be beneficial, other factors, including interest rates, liquidity and transaction costs, should also be taken into consideration. The aim should be to strike a balance that is compatible with your income goals and risk tolerance. This strategic approach helps maximize the compounding effect while ensuring that all other important elements of financial management are not affected. It highlights the need to be aware and careful in the selection of financial products to leverage compound interest over a long period of time.

Also Read: Market Making: Strategies and Techniques

– Reinvest Earnings and Dividends

Reinvesting earnings and dividends is an aggressive approach; however, it compounds wealth over time. Rather than having the profits that are made from an investment taken out, people put those earnings back into the principal amount. This act not only strengthens the first investment but also guarantees that interest calculations will be performed on a larger amount in the future. If the dividends are reinvested, especially in stocks or mutual funds paying high dividends, then there is a compounding effect that greatly increases total returns. This approach coincides with a long-term investing mentality, empowering people to enjoy the full benefits of compound interest.

The essence of reinvesting earnings lies in the fact that it gives rise to a self-perpetuating circle. When earnings are reinvested, the investment base increases, which in turn provides higher returns at a later stage. This compounding effect especially quickly builds wealth when combined with a consistent contribution strategy. Most investment platforms provide automatic DRIPs that simplify the process and help investors benefit from compounding effects without manual intervention.

– Diversify Investments

Diversification is a shrewd strategy used to distribute investments among various asset classes, industries and geographical locations. This strategy minimizes risk since poor performance in any particular investment is limited. Diversification of capital investments increases the stability of a portfolio and acts as protection from market volatility. Though diversification does not directly affect the multiplication of interest, it is essential for protecting capital accumulated against large drawdowns. Proper diversification of a portfolio ensures that the overall investment strategy remains strong, allowing compound interest to do its work in the long term without being vulnerable to the risks of concentrated holdings.

Also, diversification gives investors access to various investment opportunities. It enables them to profit from industries, asset types and locations in different proportions, balancing the general growth of an overall portfolio. This approach is consistent with a risk-conscious mindset, and the compounding effect does not get negated through the unvirtuous impacts of concentrated risk. This can be achieved by investing strategically and diversifying investments so as to ensure that an individual is well placed against market fluctuations with a view to capitalizing on the gains from compound interest over time.

– Take Advantage of Tax-Advantaged Accounts

Using tax-advantaged accounts is a savvy move towards amassing wealth through compound interest with minimal implications for taxes. Thus, accounts such as Individual Retirement Accounts (IRAS) and 401(ks), provide tax incentives, which make investments grow either on a nontaxed or deferred basis. What this implies is that the effect of compounding takes place in a period where there are no immediate tax liabilities, translating to additional funds for reinvestment and continued compounding over time. Contributions to these accounts enable people to maximize their cumulative income gains, fully utilizing the lever of compound interest.

Tax-advantaged accounts are accompanied by certain restrictions and contribution limits; therefore, understanding the rules governing these types of contributions is very important. 401(k) plans may have matching contributions from employers, making this strategy an additional benefit. All in all, the increased tax efficiency of these accounts contributes positively to compounding dynamism, thus creating a favorable environment for wealth accumulation and retirement savings.

Conclusion

In terms of saving for retirement, compound interest is especially noticeable. Starting early and saving steadily over the years allows an individual to take advantage of compounding, thus accumulating a larger retirement nest egg than without it. The compound interest’s potential for exponential growth highlights the necessity of adopting a long-term outlook, which promotes patience and endurance in people to stick with their goals. Also, the beneficiaries of investments intended to realize future goals who possess knowledge of compound interest serve as an economic force. It promotes tactical choices, including reinvesting revenues, diversifying selections and using tax favored accounts, in order to enable wealth creation.

All in all, compound interest is not just a financial notion; it’s an active agent that can define the destinies of finances. Its full potential is unlocked by patience and consistency. A comprehension of how compound interest works and the successful use thereof will put people on a path to long-term prosperity While embarking on the process of retirement planning or dealing with investments, compound interest can be used as a trusted companion, which stands for those who know its essence and make it an integral part of their financial strategies.

I craft stories that make complex ideas clear. I simplify the blend of data science, machine learning, and crypto trading, showcasing how advanced tech and quantitative models analyze data for informed trading choices. Join me in exploring the realm of quantitative trading, where my narratives make intricate concepts easy to grasp.